Laura Archange

Partner | Legal

Luxembourg - Legal Services

Laura Archange

Partner

Luxembourg - Legal Services

Luxembourg has proposed significant changes to its securitisation law that will expand structuring options and remove several practical challenges introduced by earlier reforms.

Bill of Law No. 8761 introduces changes to how securitisation vehicles can be financed, managed and structured, reinforcing Luxembourg’s position as a leading jurisdiction for securitisation and structured finance.

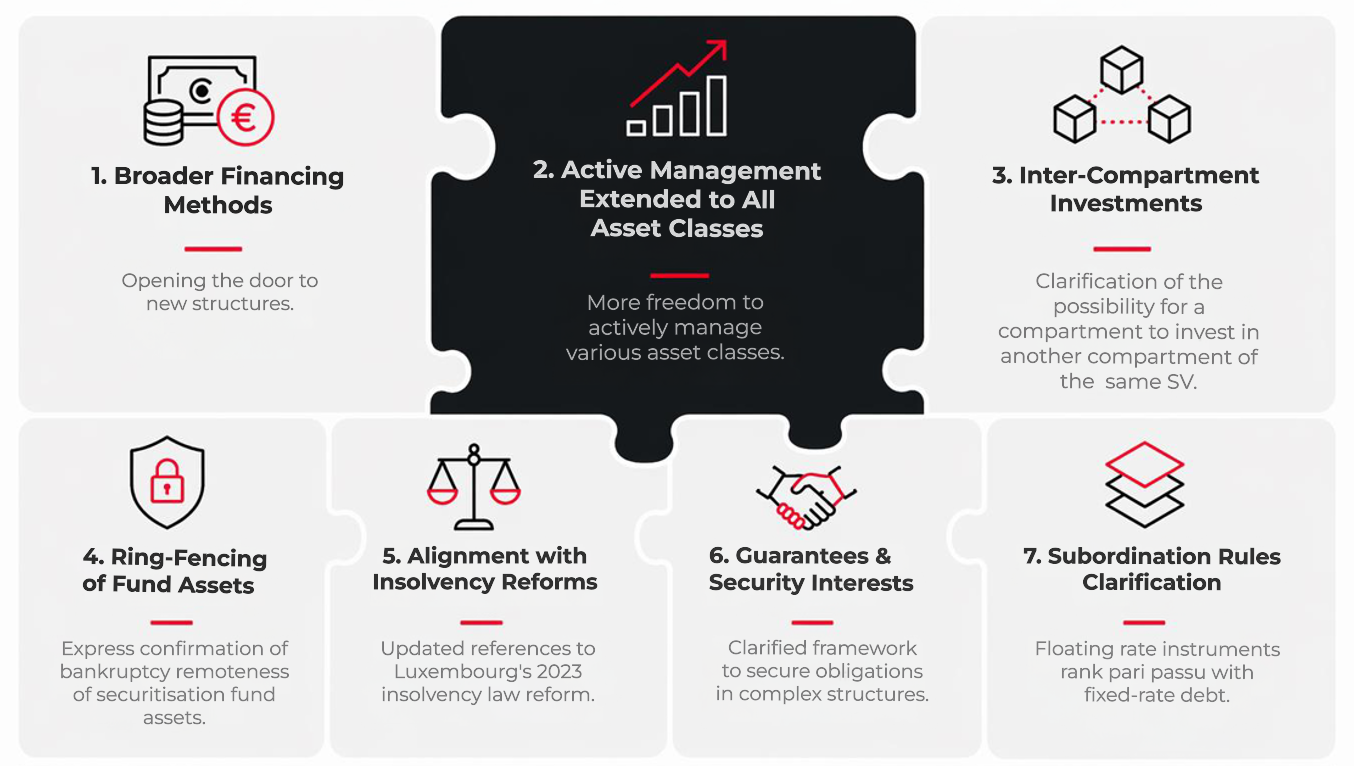

Headline changes include extending active management to all asset classes, broadening the range of eligible financing methods and clarifying the treatment of inter-compartment investments, guarantees and subordination.

Ogier recently sponsored Global ABS 2026, where conversations highlighted a clear shift in market focus towards European competitiveness, regulatory reform and the convergence between private credit, asset-backed finance and securitisation. Against this backdrop, the proposed reforms appear well-timed, supporting more flexible, multi-asset structures. Luxembourg is responding to the evolving needs of a market that is becoming broader, more sophisticated and increasingly innovation-driven.

This briefing summarises the main amendments and explains their practical implications for sponsors, originators, investors and securitisation market players.

On 8 June 2026, the Luxembourg Government submitted Bill of Law No. 8761 to the Chamber of Deputies, proposing targeted amendments to the Law of 22 March 2004 on securitisation (the Securitisation Law). The bill was approved by the Council of Government on 3 June 2026 on the proposal of the Minister of Finance, Gilles Roth.

It builds on the reforms introduced by the Law of 25 February 2022 (the 2022 Law) and responds to structuring gaps that market participants have identified since that reform entered into force.

The amendments are technical but significant. Taken together, they expand the range of eligible financing instruments, extend active management to all asset classes, introduce a statutory safe harbour for passive portfolio operations, enable inter-compartment investments, clarify the scope of permissible guarantees and security interests, update the subordination framework for floating rate instruments and align the Securitisation Law with Luxembourg's reformed insolvency regime.

The bill would amend the definition of securitisation by expanding the definition of "credit" to cover any form of financing or other financial commitment, in addition to conventional loans and financial instruments.

The 2022 Law already broadened the financing options available to securitisation vehicles (SVs) beyond the traditional securities issuance model. This bill goes further by allowing for an even broader range of financing solutions.

The bill is explicitly designed to accommodate Islamic finance structures, in particular asset-backed sukuks, for which Shariah law precludes the use of interest-bearing loans or conventional debt instruments.

Luxembourg has historically been a favoured jurisdiction for Shariah-compliant securitisation structures, given the flexibility of its multi-compartment regime and the broad range of securitisable assets. The bill removes the residual legal uncertainty for the use of Luxembourg SVs as sukuk issuance platforms. More broadly, the change means that SVs may be financed through any form of financial arrangements, in addition to loans and issuances of financial instruments.

Public issuances must still be funded exclusively through the issuance of financial instruments. This restriction, expressly inserted by the bill, ensures that retail investors are not exposed to funding structures that fall outside the conventional financial instruments framework.

The bill proposes to insert an express provision confirming that for structures set-up as a securitisation fund with a management company, the assets managed by that company on behalf of the fund(s) do not form part of the management company's estate in the event of insolvency and cannot be used to satisfy the management company's own creditors.

This amendment is modelled on the well-established principle applicable to investment funds under the Law of 17 December 2010 on UCITS. The absence of an equivalent express provision from the Securitisation Law had created a theoretical gap: while practitioners understood asset segregation to be a feature of the securitisation fund regime, its codification in the UCITS and AIFM contexts, but not in the securitisation context, left room for disagreement in an insolvency scenario.

This codification reinforces the bankruptcy remoteness of securitisation fund structures and provides a clearer legal basis for asset segregation - a key consideration for rating agencies, noteholders and investors in SVs.

The bill introduces a new article expressly authorising a compartment of an SV to invest, directly or indirectly, in one or more other compartments of the same SV. This structure mirrors what is already permissible for specialised investment funds (SIFs) under the Law of 13 February 2007 and for reserved alternative investment funds (RAIFs) under the Law of 23 July 2016. Both of these permit intra-entity compartment investments subject to anti-circularity conditions:

Where the investment is made through debt instruments, the investing compartment enjoys the full rights of a creditor, including voting rights and entitlement to financial returns.

The bill expressly disapplies Article 1300 of the Civil Code, which would otherwise extinguish obligations by confusion when debtor and creditor are the same person. This preserves the legal integrity of the investment relationship between compartments of the same legal entity.

This amendment opens the door to master-feeder structures, reducing vehicle count and structuring costs for multi-compartment platforms and bespoke mandates.

Managers running multiple asset classes within a single umbrella SV will benefit from significantly more operational flexibility.

Article 5 aims to rewrite Article 61(3) of the Securitisation Law, replacing the existing restriction on the granting of security and guarantees with a clear tripartite framework. Under the suggested revised provision, an SV may grant guarantees or constitute security interests:

The amendment gives SVs a clear statutory basis to grant security in favour of co-investors, upstream lenders and other parties involved in the transaction, removing residual ambiguity from structuring documentation.

The final provision is the most significant expansion. It expressly allows an SV to grant security in favour of a party whose exposure arises from their investment in the securitisation transaction - a common requirement in leveraged and complex structures - rather than being limited to direct transaction creditors.

The 2022 Law introduced an express statutory basis for active management of securitised assets. This was a departure from the previously prevailing view (reflected in the CSSF FAQ) that SVs were restricted to passive management. However, the 2022 Law limited active management to portfolios composed of debt securities, loans, debt financial instruments or receivables, subject to the instruments not being offered to the public.

Extending active management to all asset classes could be beneficial for European CLO and CDO issuances which use equity-linked or hybrid strategies.

The revised provision removes the asset class restriction: active management is now permissible for any risk portfolio, subject only to the condition that the instruments used to finance the portfolio are not offered to the public.

Article 7 amends Article 64(1)(5) of the Securitisation Law, which sets out the statutory hierarchy of subordination for financial instruments issued by SVs, which apply in the absence of contractual subordination provisions. The amendment clarifies that debt instruments remunerated by reference to a floating rate index plus a fixed margin (for example, EURIBOR + 200 bps) rank pari passu with fixed-rate debt instruments, and both categories are senior to instruments whose return depends on the residual performance of the SV's assets.

Prior to this amendment, the Securitisation Law referred only to "debt financial instruments with a fixed rate" as the senior category and subordinated all "non-fixed income debt financial instruments" to that category. A floating rate instrument (EURIBOR + fixed margin) was formally non-fixed in its remuneration, but was functionally equivalent to a fixed-rate instrument: the return is fully determinable at inception, irrespective of the SV's asset performance.

The official commentary to the bill explains that the equal ranking is explained by their nature, as their return is fixed or calculable in advance and does not depend on how well the underlying assets perform.

Bill 8761 is well-targeted legislation that addresses specific pain points identified by practitioners since the 2022 Law. Two amendments are of particular significance.

The bill is now before the Conseil d'État for its opinion. Ogier's Banking and Finance team in Luxembourg will monitor the legislative process closely and is available to advise on the implications of the proposed reforms for new and existing structures.

Ogier is a professional services firm with the knowledge and expertise to handle the most demanding and complex transactions and provide expert, efficient and cost-effective services to all our clients. We regularly win awards for the quality of our client service, our work and our people.

This client briefing has been prepared for clients and professional associates of Ogier. The information and expressions of opinion which it contains are not intended to be a comprehensive study or to provide legal advice and should not be treated as a substitute for specific advice concerning individual situations.

Regulatory information can be found under Legal Notice

Sign up to receive updates and newsletters from us.

Sign up