Raulin Amy

Partner | Legal

Jersey

Raulin Amy

Partner

Jersey

Complex tax, accounting and employment matters are amongst those which drive the choice of acquisition structure for private equity funded transactions. Some of the most common types of private equity acquisition transactions are the leveraged buyout (LBO) and the management buyout (MBO).

Where an LBO/MBO transaction involves a domestic or international business with a UK-domiciled management team, the use of Jersey acquisition structures has gained traction with UK private equity advisers for a number of reasons.

This briefing explains why Jersey companies, management and employee incentive plans including employee benefit trusts (EBTs) and The International Stock Exchange (TISE) quoted Eurobonds have become integral components of the LBO and MBO transaction planning process.

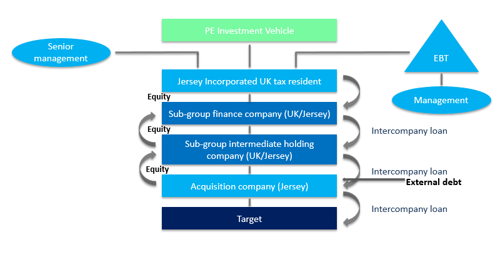

A typical Jersey debt and equity acquisition structure would comprise of:

The key Jersey-connected parts of the structure include:

Jersey group holding company/acquisition-vehicle

Jersey EBT; and a

TISE quoted Eurobond.

A tiered Jersey debt and equity holding structure:

enables structural subordination of intra-group/ acquisition financing (i.e., splits debt/equity investment)

facilitates the requirements of both the PE backer and Target group management

provides UK resident non-UK domiciled Target group management with remittance based taxation options for future exit (e.g., UK CGT)

allows for simplified dividend flows to PE investment vehicles and therefore ultimate PE investors

should not be subject to tax/stamp duty in the UK on any future disposal

the EBT (or another form of entity) facilitates the alignment of target management objectives with those of the PE shareholder

The principal advantage of using a Jersey holding company is the flexibility of Jersey company law in relation to returns to investors - whether by means of dividend, redemption of share capital or share buy-back.

A Jersey company may make a distribution from a wide range of sources, not merely from distributable profits so the concept of distributable reserves does not exist.

A zero rate of income tax applies to almost all Jersey companies (unless they are a locally regulated company, which is not necessary for this type of holding structure).

Where a Jersey company is managed and controlled in a country where all or part of the company’s income is taxed at a rate of 10% or more the company is treated as tax resident in that other country (e.g., in the UK). The effect of this is that the Jersey company should not be dual resident for UK tax purposes.

On an exit, no stamp duty is payable on the transfer of shares in a Jersey company and there is no corporation or capital gains tax in Jersey. There is also no inheritance tax in Jersey.

As an alternative exit, Jersey companies are also suitable vehicles for IPO and have been listed on all the world's major exchanges.

Rewarding, motivating and retaining senior employees and attracting new high profile executives to portfolio companies requires a well-structured, tax efficient and effectively administered remuneration package.

As part of the LBO/MBO process, it is usual for share based incentive plans to be designed to align the activities of executives and senior employees with the requirements of the PE investor.

Whilst some senior executives may take shares directly in the Jersey holding company, joint ownership (JSOP) and share plans for the wider executive and employee base are typically operated in conjunction with a standalone entity such as an EBT or a SPV. An EBT is generally an offshore trust where the trustee's duty is to act in the interests of the employees (and certain qualifying former employees) who are beneficiaries under the EBT. The SPV is created for the sole purpose to act as the nominee for management as well as share warehousing for leavers and joiners where this is deemed tax efficient.

Jersey EBTs/SPV that form part of structured LBO/MBOs fulfil a number of functions depending on the plan structure, the stage in its lifecycle and the Target company structure. Increasingly, and particularly for MBOs, UK based Employee Ownership Trusts (EOTs), run and administered offshore, are used to provide tax efficient options for shared ownership.

It is common for EBTs and SPVs to allow for multiple share plans to be managed through a single arrangement for a group of companies. They just often operate as nominee for JSOPs and vested shares, to allow a more cohesive and easier transfer of shares if required when a person is leaving.

Incentive plans for the PE management team are often more creative and can be tax efficient depending on their country of residence and domicile. Plans include structuring of carried interest, share incentives, bonus deferral and partnership interest management.

The International Stock Exchange (TISE) has seen a dramatic increase in the listing of quoted Eurobonds since December 2002 when it was designated by the UK Inland Revenue as a recognised stock exchange under Section 841 of the UK Income and Corporation Taxes Act 1988 (ICTA).

Many of these Eurobonds have been issued in connection with private equity transactions. Typically, the debt issuing entity will be a UK tax resident company formed in connection with a private equity funded acquisition.

The ICTA designation is significant because qualifying debt securities listed on the TISE are eligible for the quoted Eurobond exemption. That exemption allows an issuer within the UK tax net to make interest payments on listed securities gross ie. without deduction of UK withholding tax of up to 20%.

Other key advantages of listing on the TISE include:

unlike other European stock exchanges, the TISE is not bound by any EU Listing Directives – including the Market Abuse Regulation (MAR) – and is able to be considerably more flexible in its approach

the TISE does not require an issuer to appoint a local paying agent in the Channel Islands or for the notes to be issued in a clearing system

the TISE is aware of transaction time constraints which affect issuers and will commit to meeting an agreed transaction timetable; and

Ogier has its own listing sponsor company, Ogier Corporate Finance Limited, which is a full member of the TISE and is one of the leading sponsors, having listed more than a fifth of all securities and debt listings on TISE.

As a combined full service law firm and corporate services administrator, Ogier is able to offer a coordinated and cohesive approach to the provision of integrated legal advice and administrative services to PE clients and their onshore advisors.

This means that specialist legal, administration and listing sponsor service teams are able to assist with all offshore acquisition structuring solutions. Ogier’s full service offering is delivered seamlessly, often with a single point of contact by:

Providing:

corporate and commercial legal advice

banking advice

employee incentive and co-ownership structuring

TISE and Cayman Stock Exchange listing agent services (via Ogier Corporate Finance Limited)

Ogier is uniquely placed to deliver legal services in all time zones, allowing clients flexibility and ease of communication.

A range of factors will need to be considered before selection of the appropriate PE acquisition structuring jurisdiction (including the Target’s location, location of investors/management and suitable time zones, other external requirements eg. taxation and other regulations).

Each of the jurisdictions in which we operate - BVI, Cayman, Guernsey, Jersey and Luxembourg offers:

Economic and political stability

Flexible, independent regulatory framework

Tax neutral location

Mature, well respected legal systems

Track record of product and service innovation

Skilled and responsive workforce

In addition, Jersey, Guernsey, Cayman and BVI legal advice is offered from our Hong Kong office to the Asia Pacific region.

Our corporate administration business, Ogier Global, works closely with the partner-led legal teams in BVI, Cayman, Guernsey, Hong Kong, Jersey and Luxembourg to incorporate and administer a wide variety of vehicles. Ogier Global works closely with the legal teams to provide corporate, funds, private wealth, real estate and structured finance services.

Our highly experienced and responsive team of technical experts focuses on providing the highest level of personal service, working collaboratively with clients and delivering commercial solutions in the most efficient way.

We work with leading financial institutions, investment managers, corporations and their advisers across a range of industry sectors including funds and investment management, energy and natural resources, real estate, telecommunications, media and technology, infrastructure and healthcare.

Our services include:

Formation

Registered Office / Registered Agent

Company Secretarial

Governance Services

Accounting and Financial Reporting

Regulatory and Compliance

Trustee and nominee services for employee incentive and co-ownership structuring

Ogier provides practical advice on BVI, Cayman Islands, Guernsey, Jersey and Luxembourg law through its global network of officers. Ours is the only firm to advise on these five laws. We regularly win awards for the quality of our service, our work and our people.

This client briefing has been prepared for clients and professional associates of Ogier. The information and expressions of opinion which it contains are not intended to be a comprehensive study or to provide legal advice and should not be treated as a substitute for specific advice concerning individual situations.

Regulatory information can be found here.

Ogier is a professional services firm with the knowledge and expertise to handle the most demanding and complex transactions and provide expert, efficient and cost-effective services to all our clients. We regularly win awards for the quality of our client service, our work and our people.

This client briefing has been prepared for clients and professional associates of Ogier. The information and expressions of opinion which it contains are not intended to be a comprehensive study or to provide legal advice and should not be treated as a substitute for specific advice concerning individual situations.

Regulatory information can be found under Legal Notice

Sign up to receive updates and newsletters from us.

Sign up