Oisin McClenaghan

Partner | Legal

Ireland

Oisin McClenaghan

Partner

Ireland

Oisin McClenaghan

Team: Jennifer Dobbyn, Simon Keogh, John Perry, Dave Nolan, Laura Holtham, Margot Carty, Edwina Hilton, Arthur Gaskin

ON THIS PAGE

RELATED

The Central Bank of Ireland has substantially enhanced the Irish private assets, private credit and alternatives regulatory framework. The changes extend significantly greater flexibility to investment managers when structuring their investment funds to better meet investors’ needs.

The updated CBI Alternative Investment Fund (AIF) Rulebook became effective on 5 May 2026.

In the Central Bank of Ireland’s own words, the "Central Bank is reinforcing Ireland’s position as a leading jurisdiction for the domiciliation of alternative investment funds. These changes will support greater investor choice, maintain high standards of investor protection, reduce systemic risk and enable continued innovation in fund structuring".

The AIF Rulebook is the regulatory framework underpinning Ireland’s role as one of the world’s leading AIF domiciles.

The updated AIF Rulebook now aligns Ireland with Europe’s updated Alternative Investment Fund Managers Directive (AIFMD II) and the broader Savings and Investment Union (SIU) goals, while at the same time enhancing's Ireland’s appeal as a platform for private assets and long-term investment strategies.

The Central Bank of Ireland's reforms provide international asset managers with a significantly enhanced Irish product range, helping them deliver their private assets and direct lending strategies to market with greater efficiency and flexibility.

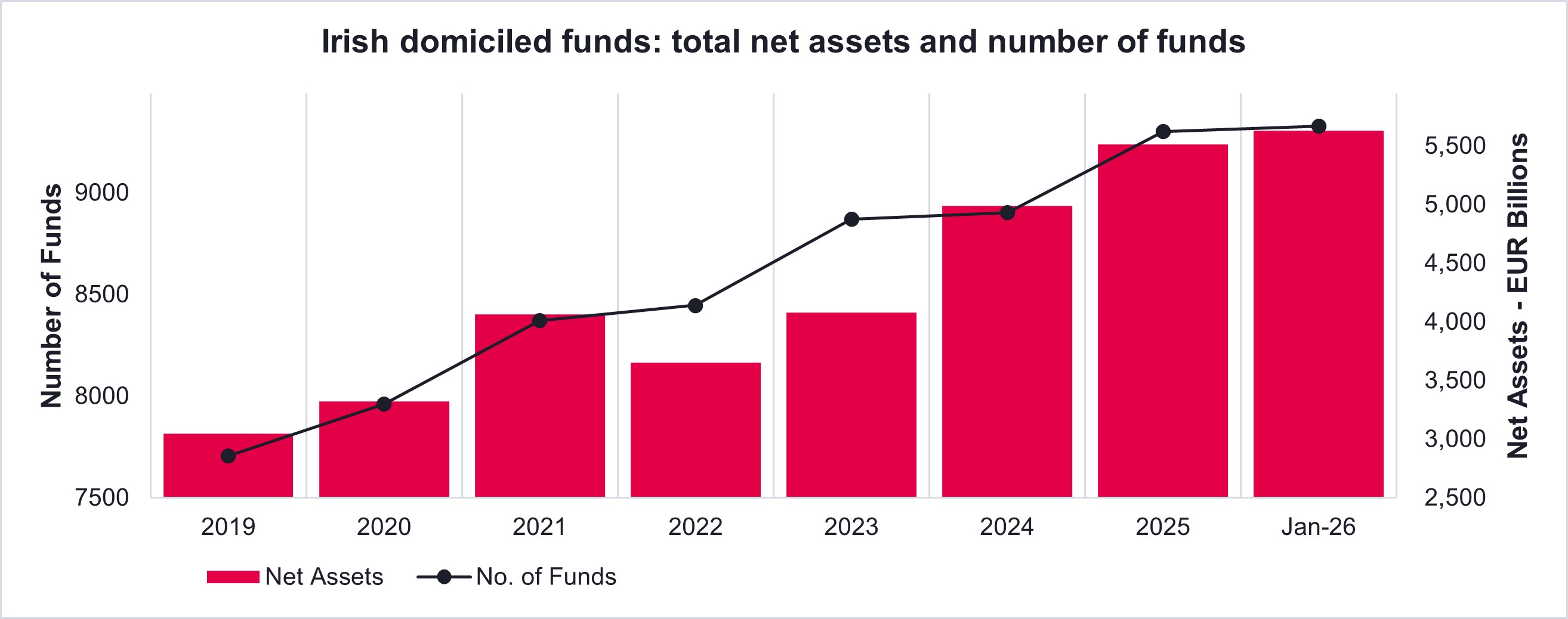

The assets under management in Irish domiciled investment funds increased by 39% in the 24 months to 31 December 2025 and now stand at over €5.6 trillion.

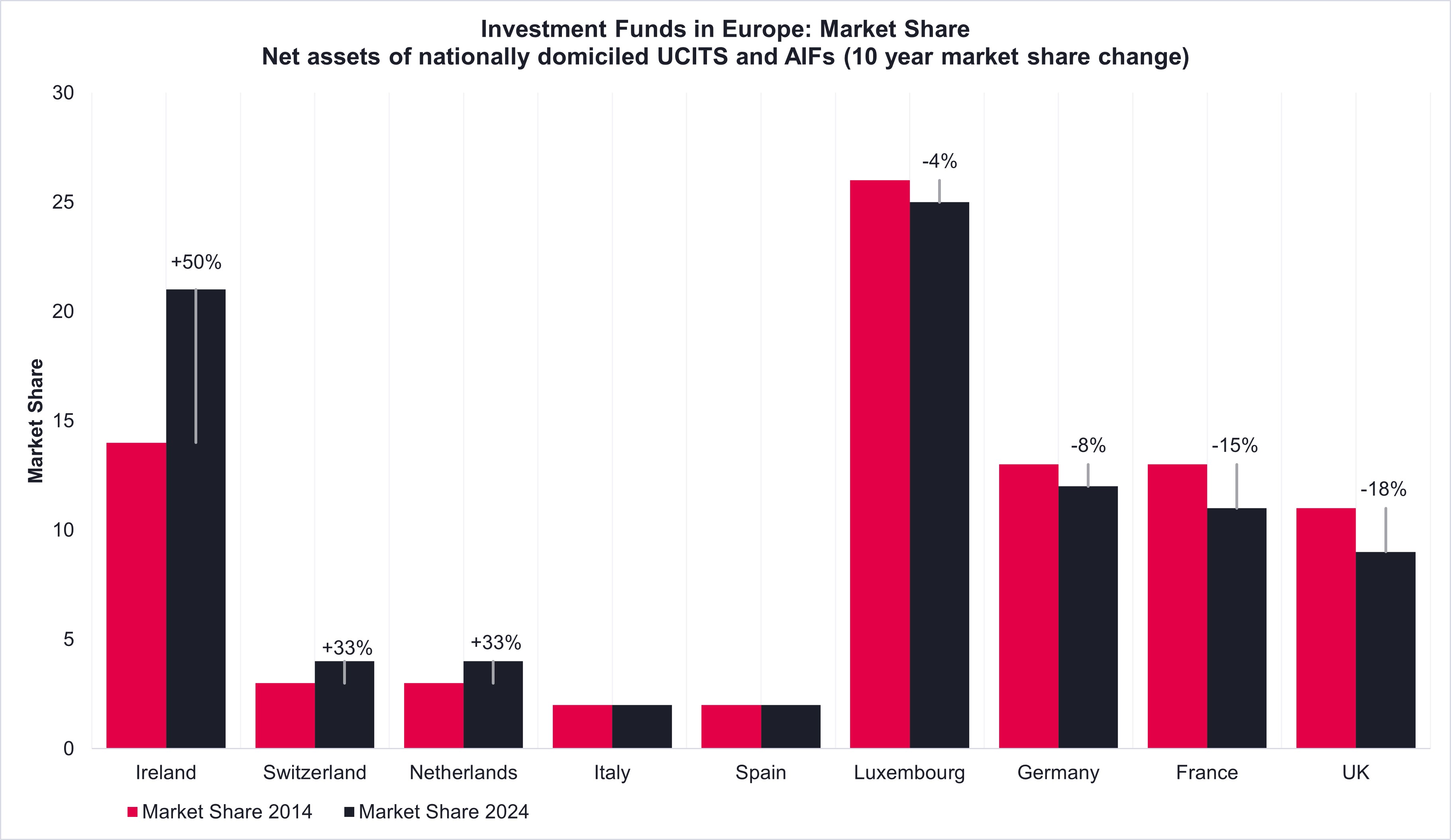

Ireland's share of the European funds market (AIFs and UCITS) has increased by 50% in the last 10 years. A substantial portion of that increase is attributable to growth in Irish domiciled AIFs. The regulatory enhancements will ensure the continuation of that upward trajectory.

Widely welcomed by stakeholders, the enhanced framework aligns the Irish regulatory landscape with evolving European rules and global standards, avoids regulatory gold plating and address the needs of modern private asset and alternatives allocation strategies. Investor protections are pragmatically and comprehensively reinforced.

|

Key changes to the AIF Rulebook |

What is proposed |

|

Loan origination |

Removal of the legacy Irish loan origination fund requirements (Loan Origination QIAIF regime), implementation of more flexible EU-wide AIFMD II loan origination rules. |

|

Liquidity management tools (LMTs) |

Incorporation of AIFMD II LMT obligations including enhanced disclosures on selection and use. |

|

Use of subsidiaries |

Replacement in full of Central Bank subsidiary rules with flexible disclosure and oversight driven regime. AIFs no longer required to be party to subsidiaries' contractual arrangements. Requirement to have certain overlapping directors at AIF and subsidiary level removed. |

|

Funds acting as third-party guarantors |

Deletion in full of restrictions on QIAIFs granting loans or acting as guarantors to third parties. The restriction of QIAIFs acting as guarantors on behalf of third parties frequently led to additional complexity in circumstances where a fund group, including a QIAIF, was entering into a credit facility. The removal of this prohibition greatly simplifies the process and provides greater fund financing options. Read more about the positive impact of the AIF Rulebook changes on fund finance in Ireland here. |

|

Reduced CBI filing obligations |

AIFs are no longer required to notify the CBI in advance of proposed amendments to the prospectus, supplement or offering memorandum, or any material agreements (including the investment management, depositary and administration agreements). |

|

Side pocketing |

The requirement for a QIAIF to classify its liquidity profile as open-ended with limited liquidity to establish side pockets has been removed. Open ended QIAIFs may also establish side pockets. |

|

Offer periods |

Removal of two-and-a-half-year cap on initial offer periods and replacement with disclosure-based approach. |

|

Excuse and exclude, stage investing and management participation enhancements |

The AIF Rulebook now explicitly provides for the allocation of asset specific returns to individual share classes and non-pro rata share class participation to optimise flexibility in connection with excuse and exclude provisions, stage investing and management participation. |

|

Charity share classes |

The creation of share classes which make distributions to charity is now provided for. |

|

Side letters |

Additional side letter flexibilities are now provided for, subject to disclosure and no material disadvantage to other investors. |

|

Significant influence |

Removal of restriction on QIAIFs, their GPs or their AIFMs from acquiring shares carrying voting rights which enable them to exercise significant influence over the management of the issuing body. This provision was already disapplied to private equity, venture capital and development capital funds but has now been disapplied to all QIAIFs, regardless of strategy, and replaced with a prospectus disclosure obligation. |

|

Greater in kind / in specie subscription and redemption flexibility |

Less proscriptive and more principal-based requirements relating to in specie subscriptions and redemptions are now provided for. |

|

Removal of 10% limit on retained redemption proceeds |

The former 10% limit on retained redemption proceeds no longer applies, replaced with an obligation to disclose such ability in the prospectus. |

|

Non-EU AIFMs |

The AIF Rulebook now specifically sets out the limited requirements applicable to AIFs with non-EU AIFMs in the AIF Rulebook (i.e., the requirements applicable to, for example, an AIF with a US investment manager designated as the non-EU AIFM of the AIF are now formally documented in the AIF Rulebook). |

|

Expedited CBI approval of Irish feeder funds into Hong Kong retail funds |

Following on from the Memorandum of Understanding (MoU) entered into between the Hong Kong Securities and Futures Commission (SFC) and the CBI in 2025, the CBI has now established an expedited CBI approval process for the establishment of an Irish feeder AIF into a Hong Kong retail fund (funds established under s. 104 of the Hong Kong Securities and Futures Ordinance). See our update on MoU here: Irish UCITS gain swifter access to Hong Kong investors | Ogier |

|

Warehousing |

Alignment with the Central Bank's ELTIF requirement, namely the requirement that a QIAIF not pay more than the current market value for warehoused assets has been removed and replaced with enhanced prospectus disclosure obligations relating to fees, charges or interest payable. |

|

Change of AIFM / depositary |

The current obligation for the constitutional document to specify the procedure for replacing a depositary and AIFM is being removed. |

|

Connected parties |

Clarification that unitholders are subject to the connected parties' rules, except in relation to their subscription/redemption activity in the QIAIF. |

|

Consistency |

Alignment of QIAIF and ELTIF chapters aims to ensure that the relevant provisions remain consistent. |

Certain fund types are likely to be particularly impacted by the changes and should take early legal advice to ensure alignment:

Private credit and loan origination funds: the former CBI loan origination QIAIF regime has replaced in full by the AIFMD loan origination requirements. AIFMD II grandfathering provisions apply to existing credit funds. New loan origination funds are subject to the updated regime. Read our guide to QIAIFs in Ireland here.

Managers using subsidiaries or intermediaries: as oversight shifts to a disclosure-based regime, new flexibilities may be availed of and new disclosure obligations will need to be considered.

Updating fund documentation: a pragmatic approach has been adopted by the Central Bank in connection with existing funds adopting any changes required to align with the new regime. Any required changes should be incorporated at the time of the next update to a fund's prospectus or offering documents.

Ireland as fund domicile of choice: Ireland is a major hub for cross border distribution and Irish funds are sold in 90 countries across Europe, the Americas, Asia and the Pacific, the Middle East and Africa. 1,007 fund promoters have chosen Ireland to domicile and / or service their funds. Talk to us about how you can leverage Ireland's comprehensive, market leading and competitive funds offering for the delivery of your strategy to end investors.

Ogier in Ireland's Investment Funds team has had a leading role in the regulatory engagement process resulting in the adoption of the updated AIF Rulebook.

Ogier in Ireland has substantial experience working with clients across a wide variety of sectors and structures, including private credit, debt, private equity, alternatives, infrastructure, real estate, healthcare, energy, technology and across the full spectrum of fund strategies.

We assist managers and promoters in delivering and maintaining their global investment strategies through Irish fund structures, including QIAIFs. Read more about our Investment Funds services in Ireland.

For further information on the QIAIF or how we can help, contact one of the team via their details below.

Partner | Legal

Ireland

Oisin McClenaghan

Partner

Ireland

Partner | Legal

Ireland

Jennifer Dobbyn

Partner

Ireland

Senior Associate | Legal

Ireland

Simon Keogh

Senior Associate

Ireland

Tax Partner | Legal

Ireland

John Perry

Tax Partner

Ireland

Counsel | Legal

Ireland

Dave Nolan

Counsel

Ireland

Partner | Legal

Ireland

Laura Holtham

Partner

Ireland

Listing Director | Corporate and Fiduciary

Ireland

Margot Carty

Listing Director

Ireland

Tax Associate | Legal

Ireland

Edwina Hilton

Tax Associate

Ireland

Tax Counsel | Legal

Ireland

Arthur Gaskin

Tax Counsel

Ireland

Ogier is a professional services firm with the knowledge and expertise to handle the most demanding and complex transactions and provide expert, efficient and cost-effective services to all our clients. We regularly win awards for the quality of our client service, our work and our people.

This client briefing has been prepared for clients and professional associates of Ogier. The information and expressions of opinion which it contains are not intended to be a comprehensive study or to provide legal advice and should not be treated as a substitute for specific advice concerning individual situations.

Regulatory information can be found under Legal Notice

Sign up to receive updates and newsletters from us.

Sign up